Blog | 19 Dec 2017

The West’s ‘new mediocre’ and the rise of China’s economics

In a recent article ’The Arrival of the Century of Chinese Economics’ Justin Yifu Lin argued that the centre of world theoretical economics would pass to China:

‘I also made a prediction… in the 21st century it is quite possible that many master economists will emerge through the study of China’s economy….

‘The importance of a theory depends on the importance of the phenomenon explained by the theory. If the phenomenon to be explained is important then explaining a phenomenon, and revealing the causal logic behind it, makes this an important theory.

‘What is an important phenomenon? Phenomena occurring in important countries are an important ones. Considering the history of the development of modern economics, Adam Smith published the Wealth of Nations established modern economics. From the late eighteenth century until the mid-twentieth century, the centre of world economics, of significant contributions to economics, was the United Kingdom The vast majority of leading scholars were British or foreign economists working in the United Kingdom. After the 1940s and 1950s, the vast majority of economists who made major contributions to economics were American economists who worked in their United States home or were foreign economists working there….

‘After World War I, the centre of the world economy moved to the United States. The most important economic phenomena are the phenomena appearing in the centre of the world economy. With the transfer of the centre of the world economy, the research centre for world economics also followed.

‘In terms of purchasing power parity [PPP], China became the world’s largest economy in 2014. As long as China’s steady development continues, then at market exchange rates it is very likely that China will become the world’s largest economy by 2025. At present, China’s accounts for 18% of the world’s economy and this will be more than 20% by 2025. By 2050, China’s economy is likely to account for between 25% and 50% of the world economy…. China will be the most important centre of the world economy and the centre of world economics may shift from the United States to China. …

‘It is very likely that we are witnessing the arrival of a new era that is of great importance to humankind because China is became a middle-income country, from one of the world’s poorest countries, and it will become In a high-income country. Most of the countries in the world now are developing countries – low income… countries and… middle-income countries. The have the desire to modernize and become high-income countries. It is therefore necessary to summarize the theoretical innovations made in China’s economic experience, and develop better ways to test the contribution of these theories.’

Indeed, in order to achieve the fastest sustained growth in a major economy in human history. China has already had to pass through decisive tests of the superiority of its economic thinking. Most fundamentally, from the positive, the ‘socialist market economy’ created by Deng Xiaoping, Chen Yun and their collaborators was unprecedented in human history – an intellectual and theoretical achievement of the highest order. This is analysed at length in my book The Great Chess Game and in a popular fashion in an article whose title is self-explanatory ‘Deng Xiaoping: the World’s Greatest Economist‘.

China’s success was necessarily not merely practical but theoretical because its policies were carried out in clear opposition to dominant orthodox Western economic theory, and with China putting forward its own economic concepts. As Justin Lin Yifu noted:

‘There was a [Western] consensus that the economic results of the gradual and twin-track policy that China carried out would be worse… But now, looking back, China is the fastest-growing and most stable economy in the past four decades. Countries that have undergone a restructuring by Washington’s consensus shock therapy have experienced a crisis of economic collapse and stagnation. ‘

But if China’s theory of the ‘socialist market economy’ was demonstrated to be superior to those in the West ‘from the positive’ by China’s own economic growth it was also shown to be correct ‘from the negative’ not only in developing countries but in particular by application of dominant Western economic theories in the former Soviet Union. The application of these after 1991, in ‘shock therapy’, produced in the Russia the greatest economic collapse in a major economy in peacetime since the Industrial Revolution with a decline of GDP of 39% in a seven-year period. It was entire possible to predict this disaster in advance, as shown in my article written in April 1992 ‘Why the Economic Reform Succeeded in China and Will Fail in Russia and Eastern Europe’ This article, originally published in Russian, reflected the fact that from 1992-2000 the present author lived in Moscow attempting to persuade the Russian authorities to adopt the approach of China’s economic reform instead of the disaster of Western economics’ ‘shock therapy’. It may be noted that this article was written entirely from the point of view of economic theory, as at that time I had never visited China, nor did I have direct contact with Chinese economists – although I carefully studied material available in the West of Deng Xiaoping, Chen Yun and works on Chinese economic theory.

My agreement with the views of Justin Yifu Lin on the superiority of China’s economic thinking, and of his assessment of the movement of the centre of global economic thinking to China, is therefore not based on recent events but on more than a quarter century of study of China’s economy theory and practice and comparison of its results with dominant ideas in the West.

The present situation of the world economy

Within the overall historical framework outlined above, the aim of the present article is to make a more fine-grained analysis of the present situation – to show that the present situation of the global economy, more specifically of trends in the G7 economies, makes it more urgent to reinforce and speed up a transition of the centre of international economic thinking to China’s ‘socialist market economy’. This is due to the fact that, as will be shown, what was referred to by IMF Managing Director Christine Lagarde as the ‘new mediocre’ in the Western economies is now characterising an entire period of the world economy. More precisely, it will be shown in detail that while the downturn in the advanced G7 economies after the international financial crisis was not as violent as during the Great Depression after 1929, the extremely slow growth that has resulted from the financial crisis has now produced a situation where overall G7 growth is actually slower than in the Great Depression. This situation necessarily has not only economic but geopolitical and domestic political consequences in the G7 – which are briefly mentioned at the end of this article. In order to avoid misunderstanding it should be made clear that while a number of Chinese writers have studied the general historical shift of the centre of economic thought to China the analysis of the present situation of this trend, in relation to the West’s ‘new mediocre’, does not imply their agreement with this specific analysis.

To establish the facts regarding global economic trends, and avoid any suggestion of adopting data excessively favourable to China, the source used for analysis here is the projections for the next five years of the world economy issued twice yearly by the IMF. These indicate essentially the same dynamic for the Western G7 economies as the present author already analysed for the US in ‘Why the US Remains Locked in Slow Growth’Why the US remains locked in slow growth‘ – that is, the IMF predicts there will be a moderate cyclical upturn in the G7 economies 2017-2018 but that this will not turn into a strengthening boom. Instead over a five-year total G7 growth will be low with an economic slowdown in 2019-2020.

Detailed analysis of macro-economic trends confirms that the reasons for the limited scope of the upturn in the G7 economies is the same as in the US. However, detailed presentation of such analysis will be given separately. The aim of the present article is simply to outline the factual predictions of the IMF and to show their implications.

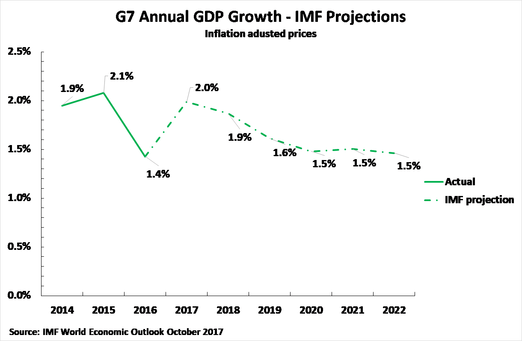

IMF predictionsTurning to trends in the global economy, the IMF’s predictions for the next five years economic growth in the G7 economies are shown in Figure 1. As may be seen, after very low growth in 2016, only 1.4%, the IMF predicts growth in 2017 of 2.0% and in 2018 of 1.9% – a moderate but real upturn. However, G7 growth is then predicted to fall to 1.6% in 2019, and to a poor 1.5% in 2020-2022. The IMF’s projection is therefore a pattern of ‘two good years and then four poor ones’.

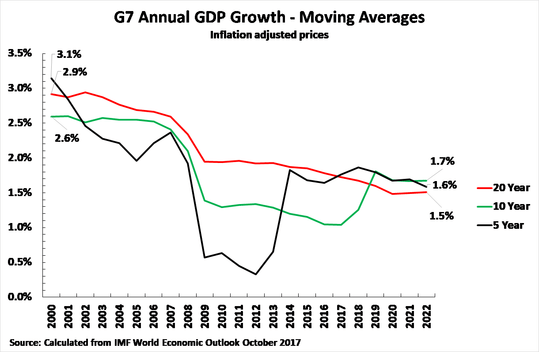

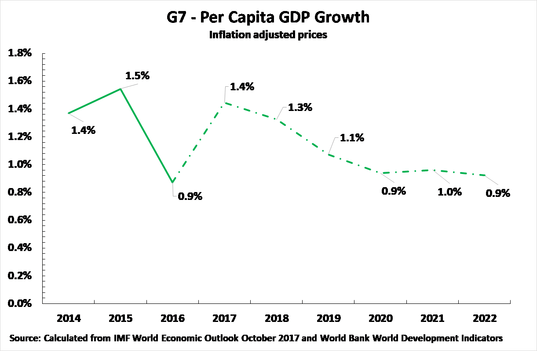

Naturally a shorter term five year moving average shows a great cyclical impact of the sharp fall in output during the 2008-2009 international financial crisis, whereas this cyclical effect is almost removed by a long term 20 year moving average, but the fundamental trend of very slow growth, particularly compared to previous performance, is clear whichever period is taken:

- Over a five-year period, annual average growth in the G7 economies is projected by the IMF to fall from 3.1% in 2000 to 1.6% in 2022.

- Over a ten-year period, annual average growth in the G7 economies is projected by the IMF to fall from 2.9% in 2000 to 1.7% in 2022.

- Over a twenty-year period, annual average growth in the G7 economies is projected by the IMF to fall from 2.9% in 2000 to 1.5% in 2022.

In summary, all averages show a severe fall in G7 annual average growth since the beginning of the 21st century and show growth rates of only 1.5%-1.7% in the next five years.

Consequently, the IMF is not projecting that the ‘new mediocre’ was a short-term trend which will be overcome but that it will continue throughout the next five years. The upturn in 2017-2018 is therefore purely cyclical and will not be consolidated into a new longer ‘boom’ – the IMF projects G7 growth will weaken again after two good years.

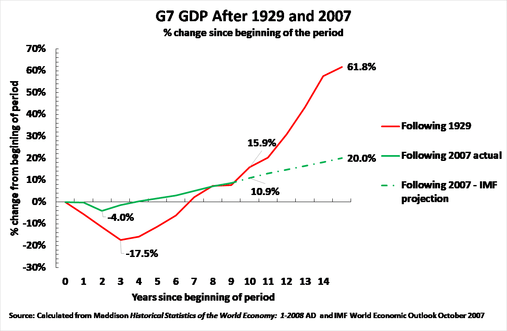

Geopolitical consequencesTo take a comparative historical framework to consider present trends it is useful to make a study of present trends in relation to the most well-known of all global economic crises – the ‘Great Depression’ after 1929. Figure 3 therefore shows the yearly development of GDP in the G7 after 1929 and 2007 (i.e. 1930 is one year after 1929, 2008 is one year after 2007 etc). This shows clearly the following key dynamics of the situation after 2007 compared to that after 1929.

- The fall in output after 1929 was far more severe than after 2007 – the maximum fall in G7 GDP after 1929 was 17.5% compared to 4.0% after 2007.

- However, after the initial severe downturn, overall growth in the G7 economies in the period after 1929 was far more rapid than after 2007. The cumulative result is that by 10 years after the initial crisis overall growth in the G7 economies after 1929 was 15.9% compared to only 10.9% after 2007. This means that by the end of 2017 overall growth in the G7 economies, after the international financial crisis, will actually be slower than during the ‘Great Depression’.

- The overall slower growth of the G7 economies after 2007 than after 1929 will become progressively more pronounced due to the very slow growth projected by the IMF. By 2022, that is 15 years after 2007, total GDP growth in the G7 economies will only be 20% compared to 62% in the 15 years after 1929.

To conceptualise this situation whereby overall G7 growth after the international financial crisis will actually be slower than after 1929 then, if the post-1929 situation is referred to as the ‘Great Depression’, then by analogy the new mediocre may perhaps be referred to as the ‘Great Stagnation’.

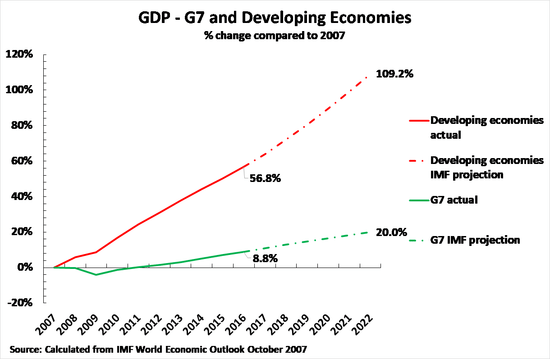

Economic and geopolitical consequencesFinally, to briefly deal with the economic and geopolitical consequences of these trends, it must first be made quite clear that the above analysis is of the trends in the G7 advanced economies. It is not an analysis of the overall trends in the world economy. Indeed, a key feature of the projections of the IMF is that far faster growth in developing economies than in the G7 will continue as shown in Figure 4.

- Over the entire period from 2007-2022 growth in the developing economies is projected by the IMF to be 109% compared to only 20% in the G7.

- Over the period 2016-2022 the IMF projects growth in the G7 to be only 10% compared to 33% in the developing economies.

Therefore, the ‘new mediocre’, is a specific feature of the G7 economies not of other parts of the world economy. In particular while low growth, the ‘new mediocre’, will continue in the G7 economic growth in developing countries will be more rapid – with annual average growth in developing economies in 2016-2022 being projected to be 4.9% compared to only 1.7% in the G7. Furthermore, the IMF projects that 44% of this growth in developing countries, almost half, will be in China itself. China’s key practical international economic projects, such as One Belt One Road, clearly fit within this framework.

The conclusions for China that follow from these international economic trends are both practical and theoretical.

First, the specific feature of any situation must be understood. As Xi Jinping quoted the Chinese philosopher Mencius: ‘As early as over 2,000 years ago, the Chinese people came to recognise that “it is natural for things to be different.”’[1] Put in terms of European thought it is the words of the Greek philosopher Heraclitus, also over 2,000 years ago, ‘No man ever steps in the same river twice’ – everything which exists is unique both in time and place. Because the most famous crisis in world economic history, that in 1929, saw an extremely rapid economic decline, whereas after World War II there was for a for prolonged period a boom, this can create the false impression that the economy must either be in a state of rapid decline or it will be in ‘boom,. However, the specific character of the present situation in the G7 economies is neither of these – it is a very long period of slow growth, a ‘new mediocre’.

Second, within this overall situation of very slow average growth business cycles still exist. The extremely low growth of the G7 economies in 2016 is therefore logically followed by faster growth in 2017-2018 – the G7 economies are oscillating around their low growth path. What the ‘new mediocre’ does mean, however, is that such upturns are temporary and do not turn into prolonged strong booms. The IMF’s projection of a new downturn in growth in 2019-2020 is therefore precisely an expression of the ‘new mediocre’.

Third, this ‘new mediocre’ inevitably means both geopolitical instability and domestic social and political instability within G7 countries.

Fourth, errors of dominant Western economic theory, of neo-liberalism, which were already shown in the stagnation produced in developing countries in the 1980s, and in the severe economic decline in the former USSR in the 1990s, are again confirmed in the inability of the G7 economies even after a decade to escape from the ‘new mediocre’. Influence of such provenly false ideas in China is therefore also dangerous for China both from the point of view of economic policy and of social stability.

Fifth, to return to this article’s starting point, the situation of the prolonged ‘new mediocre’ in the G7 economies represents part of the transition of the centre of economic thought to China. China’s rapid post-1978 economic development was created by a new economic theory, which became the ‘socialist market economy’ which had no precedent in any country and which proved its correctness through China’s unprecedented economic growth. The correctness of this economic theory was then further confirmed by the failure of Western economic theory in the ‘Washington Consensus’ for developing countries and of ‘shock therapy’ in Russia and the former USSR. The correctness of China’s concepts deriving from these concepts is now being demonstrated again in comparison to the ‘new mediocre’ resulting from the application of dominant Western economic theories in the G7.

Sixth, the spread of initiatives which follow from China’s ‘socialist market economy’ are widely understood to be increasingly crucial globally – the Belt and Broad Initiative (BRI), the Asian Infrastructure Development Bank and others. This also applies to China’s leading role in the struggle against climate change – particularly since US announcement of withdrawal from the Paris Climate Accord. But these are also part of China’s increasing international ‘thought leadership’ – BRI goes beyond the ‘free trade agreement approach’ of US sponsored post World War II trade deals to take in infrastructure and other investment, China’s increasingly leading role on climate change is an expression of its concept of a ‘community of common destiny’. Naturally such an approach has its greatest mass international impact when articulated by China’s political leaders, as for example in the wide international praise given to Xi Jinping’s speech on globalisation at the Davos World Economic Forum analysed in ‘How Xi Jinping’s Marxism Out-thinks the West ’How Xi Jinping’s Marxism out-thinks the West‘.

But while economists naturally do not have the same mass impact as state leaders this increasing impact of China’s thinking is also clear the more narrowly defined sphere of economics. ‘Classical’ works of China’s economic policy, of the period of launching of its economic reform, have of course for a long period been readily available outside China. But China’s economic success, and the cumulative impact of this in contrast to very slow growth in the West’s ‘new mediocre’, mean products of China’s contemporary economic thinking are also increasingly regularly translated and known among non-Chinese economists – for example Yu Yongding’s column on the prestigious Project Syndicat has appeared for seven years but he is now is frequently quoted in Western mass media on financial issues, Hu Angang’s books on green growth and related issues are translated, numerous works by Justin Yifu Lin on economic development which led to his Centre for New Structural Economics and Institute of South-South Cooperation are available internationally. I know directly from work in Chongyang Institute for Financial Studies, Renmin University of China the increasing international impact and connections of China’s think tanks. But numerous important Chinese economists are not yet available outside China. The combination of very low growth in the advanced Western economies and continued growth in China, is progressively speeding up overcoming this situation.

The G7 ‘new mediocre’ is therefore not merely important in its practical consequences for the world economy: the increasingly proven inability of Western economic thinking to overcome the ‘new mediocre’ is helping create the shift of the centre of world economic theory and thinking to China. As the G7 is incapable of overcoming this very slow growth, the ‘new mediocre’ in the G7 economies means this shift of the centre of international economic practice and thinking to China will intensify.

[1] Xi, J. (2014). Exchanges and Mutual Learning Make Civilizations Richer and More Colorful. In J. Xi, The Governance of China (Kindle Edition) (pp. Location 3797-3909). Beijing: Foreign Languages Press.